Introduction

Housing affordability has become one of the biggest challenges facing young families, new immigrants, and first-time homebuyers in Canada. In major metropolitan areas like Vancouver and Toronto, the dream of homeownership often feels increasingly out of reach. With rising home prices, high rent, and escalating living costs, many individuals are beginning to question whether starting life in one of Canada’s largest cities is the best financial decision.

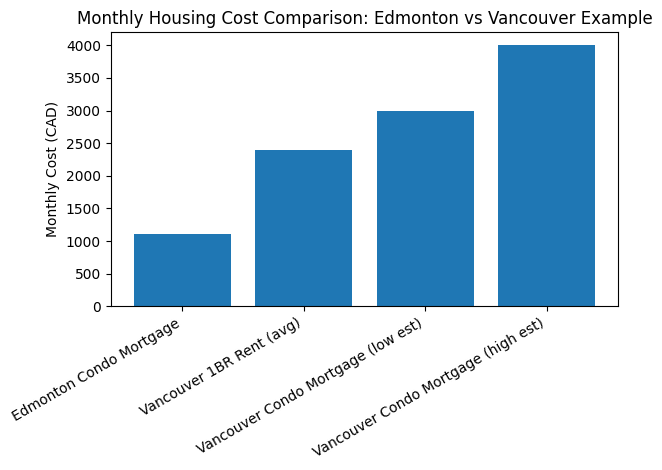

Recently, a real estate transaction highlighted a powerful example of how different the housing market can be outside major metropolitan centers. A client purchased a two-bedroom condominium in Edmonton for approximately $250,000. Their monthly mortgage payment is around $1,100 — a figure that would barely cover a parking spot or partial rent in cities like Vancouver or Toronto.

This comparison raises an important question: could starting life in a smaller Canadian city be a smarter financial strategy for young families and individuals looking to build stability and wealth?

The Housing Affordability Gap in Canada

Canada’s housing market has seen dramatic changes over the past decade. Major cities such as Vancouver and Toronto consistently rank among the most expensive housing markets in North America. According to multiple housing reports, average home prices in these cities often exceed $1 million for detached homes and remain extremely high even for condominiums.

For first-time buyers, this creates several barriers:

- Large down payment requirements

- High monthly mortgage payments

- Stricter mortgage qualification rules

- Limited ability to save or invest

In contrast, smaller Canadian cities and regional markets often offer significantly more affordable housing options. Cities like Edmonton, Calgary, Saskatoon, Winnipeg, and many communities across Atlantic Canada provide opportunities for homeownership at prices that are still accessible for many middle-income earners.

A Real Example: Buying a Home in Edmonton

Consider the example of a two-bedroom condo purchased in Edmonton for $250,000. With today’s interest rates and typical mortgage structures, the monthly mortgage payment comes out to approximately $1,100.

To put that into perspective:

- Average rent for a one-bedroom apartment in Vancouver often exceeds $2,400 per month.

- Even a modest condo mortgage in Vancouver can easily reach $3,000–$4,000 per month.

- Toronto faces similar affordability pressures.

The difference between paying $1,100 versus $3,000+ each month dramatically changes a person’s financial trajectory.

Financial Advantages of Smaller Cities

Starting life in a smaller or mid-sized city offers several financial advantages that are often overlooked.

1. Lower Housing Costs

Housing is typically the largest expense in any household budget. When mortgage payments are significantly lower, individuals have far greater flexibility with their finances.

Lower housing costs allow homeowners to:

- Build equity faster

- Reduce financial stress

- Maintain emergency savings

- Invest in other assets

2. Greater Ability to Save and Invest

When living expenses are lower, individuals can allocate more of their income toward long-term wealth building. This may include:

- Retirement savings

- Investment portfolios

- Education funds

- Starting a business

Over time, the compounding effect of saving and investing can make a significant difference in financial stability.

3. Comparable Income Opportunities

While major cities may offer slightly higher salaries in certain industries, many professions earn similar wages across Canada. In fields such as healthcare, education, trades, technology, and government services, income differences between large and mid-sized cities are often smaller than people expect.

When income remains similar but living costs are dramatically lower, individuals retain more disposable income each month.

4. Improved Quality of Life

Smaller cities can also offer lifestyle advantages including:

- Shorter commute times

- Less congestion

- More access to nature

- Stronger sense of community

- Lower daily stress levels

For many families, these benefits contribute to a higher overall quality of life.

The Psychological Barrier of Leaving Major Cities

Despite the financial advantages, many people hesitate to move away from large urban centers. Major cities offer cultural attractions, extensive public transportation, diverse job markets, and vibrant social scenes.

However, the long-term financial trade-off can be significant. Living in an expensive city often means spending a larger portion of income on housing and basic living expenses, leaving less room for financial growth.

For young professionals and families who are just beginning their financial journey, the opportunity to purchase an affordable home and begin building equity may outweigh the perceived advantages of big-city living.

Building a Strong Financial Foundation

Purchasing an affordable home in a smaller city can provide a powerful financial foundation. Over time, homeowners build equity through mortgage payments while benefiting from potential property appreciation.

Additionally, the lower monthly cost structure enables households to:

- Pay down debt faster

- Increase savings

- Invest in other opportunities

- Prepare for future financial goals

Once financial stability is achieved, individuals may later choose to relocate to larger cities with a stronger financial position.

A Strategic Approach to Homeownership

Instead of immediately targeting the most expensive housing markets, many financial advisors suggest a step-by-step approach to homeownership.

This strategy may include:

- Purchasing an affordable property in a smaller market.

- Building equity and savings over several years.

- Leveraging that equity to upgrade or relocate later.

This method allows individuals to participate in the housing market earlier while minimizing financial pressure.

The Future of Canadian Housing Choices

With remote work becoming more common and infrastructure improving across the country, the appeal of smaller cities continues to grow. Many Canadians are beginning to recognize that opportunity and quality of life are not limited to the largest urban centers.

Communities across Canada are investing in economic development, technology hubs, and improved services, making them increasingly attractive places to live and work.

As a result, housing demand in mid-sized cities may continue to rise, presenting opportunities for those who enter these markets early.

How Mortgage Strategy and First‑Time Buyer Programs Can Help

For buyers considering smaller cities, having a clear mortgage strategy and understanding available government programs can make a significant difference. Many first‑time buyers assume that purchasing a property requires a large down payment or complex financing, but Canada offers several structured pathways designed to help new homeowners enter the market.

Strategic planning allows buyers to evaluate affordability, choose the right mortgage structure, and take advantage of available programs that reduce financial pressure during the early years of homeownership.

For example, developing a well‑structured mortgage strategy and financial plan can help buyers understand how much they can comfortably afford, how to structure their loan term, and how to accelerate equity growth over time. Readers who want a deeper understanding of this process can explore this guide on mortgage strategy and financial planning which explains how to structure a mortgage in a way that supports long‑term financial stability.

In addition, many buyers overlook the variety of incentives designed specifically to help new homeowners. Programs such as tax credits, government savings plans, and buyer incentives can significantly reduce the financial barrier to entering the market. A helpful overview of these opportunities can be found in this detailed resource about first‑time home buyer programs in Canada, which explains how new buyers can leverage these programs to make homeownership more accessible.

Together, a strong mortgage strategy combined with the right first‑time buyer incentives can dramatically improve affordability, especially when purchasing in smaller Canadian cities where housing prices remain more reasonable.

How These Resources Help Homebuyers

| Topic | What It Covers | Why It Matters for Buyers in Smaller Cities |

|---|---|---|

| Mortgage Strategy & Planning | Explains how to structure your mortgage, evaluate affordability, plan long‑term finances, and select the right mortgage product. | Buyers purchasing lower‑cost homes can optimize their payments and potentially pay off their mortgage faster while building equity. |

| First‑Time Buyer Programs | Details government programs, incentives, tax credits, and savings tools designed for new buyers. | Programs can reduce the upfront financial burden, making it easier for individuals and families to enter the housing market earlier. |

When combined with the affordability advantages of smaller Canadian cities, these tools can dramatically accelerate a buyer’s path toward financial stability and homeownership.

Final Thoughts

For many individuals starting their lives in Canada — including young professionals, new immigrants, and growing families — the decision of where to live can have a profound impact on long-term financial success.

While cities like Vancouver and Toronto offer exciting opportunities, they also come with exceptionally high living costs. Smaller cities such as Edmonton demonstrate that homeownership and financial stability are still achievable within Canada.

A mortgage payment of approximately $1,100 for a two-bedroom condo represents more than just affordable housing. It represents the ability to save, invest, and build a stronger financial future.

For those looking to establish themselves in Canada, starting in a smaller city may not only be practical — it may be one of the smartest financial decisions they can make.

Frequently Asked Questions About Buying Homes in Smaller Canadian Cities

Is it cheaper to buy a home in smaller Canadian cities?

Yes. Many smaller and mid-sized cities across Canada offer significantly lower home prices compared to major markets like Vancouver and Toronto. Cities such as Edmonton, Winnipeg, and Saskatoon often provide opportunities to purchase homes or condos at a fraction of the cost of large metropolitan areas, making them attractive options for first-time buyers.

Can first-time home buyers afford property more easily outside major cities?

In many cases, yes. Lower property prices combined with government incentives and first-time buyer programs can make homeownership much more accessible in smaller markets. Lower monthly mortgage payments also allow buyers to save more and build equity faster.

Do smaller Canadian cities offer good job opportunities?

Many industries such as healthcare, trades, education, and technology provide comparable salaries across Canada. When income levels remain similar but housing costs are lower, individuals often enjoy greater financial flexibility and a better quality of life.

Is buying a condo in cities like Edmonton a good investment?

Affordable markets allow buyers to enter the housing market earlier and begin building equity. While appreciation rates may vary by city, owning property instead of renting can help build long-term financial stability.

What programs help first-time home buyers in Canada?

Canada offers several programs designed to help first-time buyers, including tax credits, savings programs, and government incentives. Understanding these programs and combining them with a smart mortgage strategy can make entering the housing market significantly easier.